Through document automation, the finance sector improves compliance standards, as well as manages to decrease costs and speed up internal processes. In this interview with Katarzyna Wódka – an innovation partnership expert from Pekao Bank – we discuss the idea of collaborations between start-ups and corporations from the world of finance.

Hi Kasia, it’s a pleasure to have the chance to chat. Before we begin to talk about Pekao and your initiatives there, let’s start with your profile – how did your career in the financial sector start?

Great to meet you too!

So, about me – I have worked in the start-up community for about 8-9 years, constantly revolving around start-ups and observing them from different perspectives: firstly, from the standpoint of a venture capital fund, later running an accelerator program and then building start-up for corporation. Finally, I joined the Innovation Lab at Pekao Bank a year and a half ago.

What can you tell us about the Innovation Lab at Pekao Bank, then? What is it that you guys do within the organization?

The primary purpose of the Pekao Innovation Lab is to support the bank in building a modern, innovative business.

I am part of the innovation partnership team, which focuses strictly on working with start-ups. Our primary goal is to connect with them and pilot their solutions for further deployments in various bank departments.

In more detail – we are responsible for finding start-ups, verifying their capabilities, then linking them with the product owners at Pekao Bank to facilitate their joint efforts. Think of it as a support unit for the bank. We look for needs internally in business departments and offices, trying to create space for innovation.

Once they are identified, we begin our market research and seek the best providers of these cutting-edge solutions. Our team conducts the whole process – from searching and verification to initiating first conversations. Then we work on these possibilities with the product owners and support them in decision-making and implementing the chosen solutions.

Is that the same process that led to the collaboration with Alphamoon?

The story with Alphamoon began last year. We started our first mutual collaboration through an accelerator program, Scale Up – an accelerating initiative Huge Tech ran as part of the IdeaGlobal. We aimed to connect the bank’s needs with selected start-ups.

As a result of this initiative, two departments approached us independently in reference to OCR (Optical Character Recognition) – the operations department and the department related to credit risk. After conducting market research, we provided a selection of four start-ups for both projects.

What were these projects about? What type of documents?

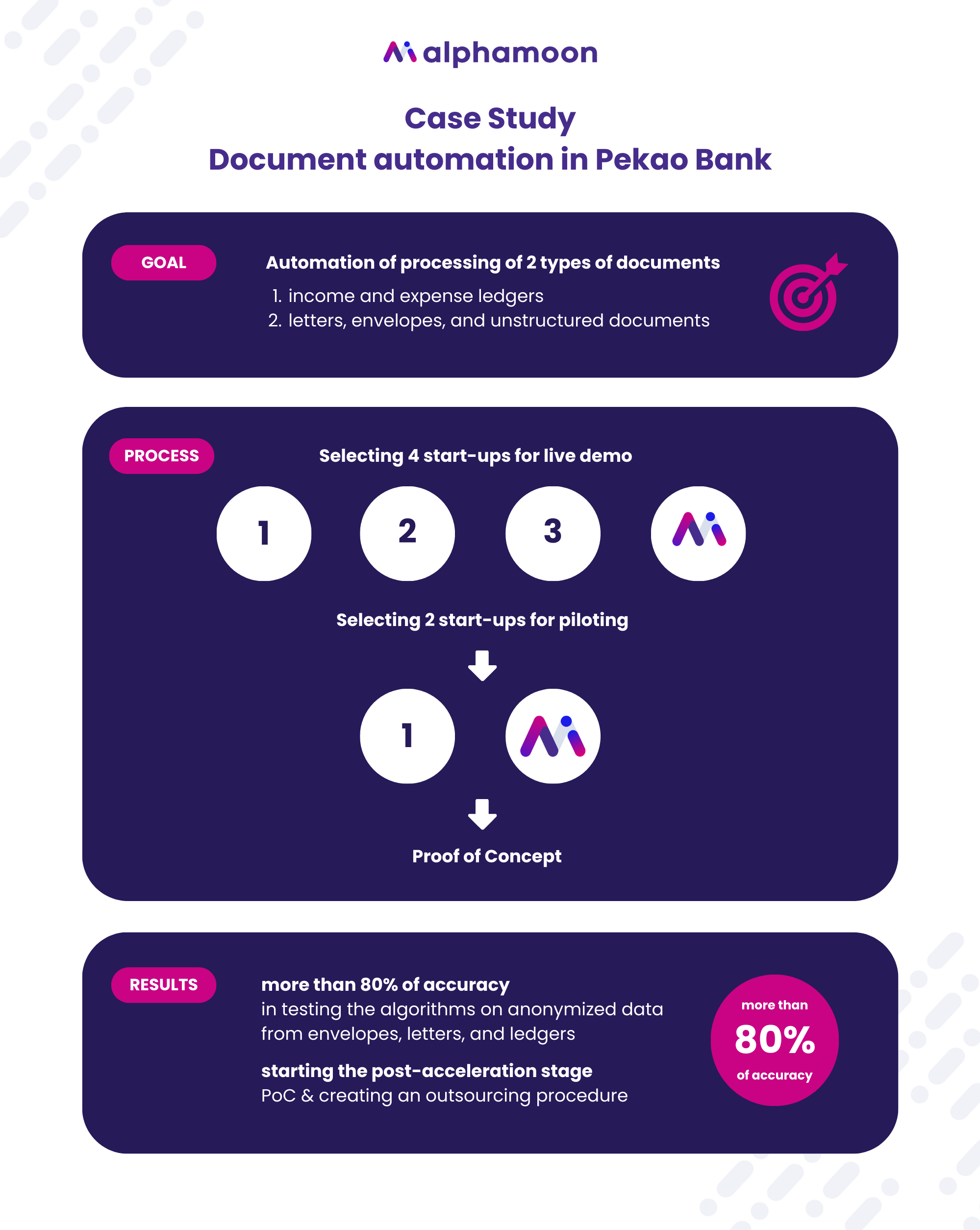

We wanted to automate the processing of 2 types of documents: the first package was income and expense ledgers, and the second one – letters, envelopes, and unstructured documents.

Those four selected start-ups had to prepare a live demo. In order to test the tech capabilities of these solutions, we tested how these tools handled reading data from PITs (tax reports). Based on such a test, we selected two entities for piloting: one of them is Alphamoon. We wanted to see how the two different algorithms performed and compare their efficiency in reading documents. The metrics we used were the reading level, errors, and the degree of human supervision required. Following that kind of methodology enabled the Pekao Innovation Lab to carefully build a business use case and recommend technology that fits the needs of the departments.

Can you share a bit more detail on the process? Did you work on the documents provided by the two departments?

Initially, as part of the acceleration phase, we completed testing the algorithms on anonymized data from envelopes, letters, and ledgers. The result was more than 80% of accuracy.

Having that score, we could move to the post-acceleration stage – PoC (proof of concept), which involves creating an outsourcing procedure. It was necessary to train the model with accurate, real data, and since we are a financial institution under rigorous supervision from regulators, we had to launch this procedure.

Frankly, this procedure is a very long and complicated.

Interesting. So time is, in fact, your most significant pain point?

It’s inconvenient for us, that’s for sure.

Testing on anonymized data is a different story than using actual client data to improve the tool’s efficiency. Working with real data under strict GDPR and data processing rules is quite challenging, and currently, we need the option to use accurate data during testing. It would be much simpler if algorithms did not require real data, but that would mean lower accuracy too.

I see. You have mentioned data accuracy as the leading metric that you use. What are the other metrics of success for the implemented solutions?

We have yet to determine the exact metrics, such as the expected number of documents we have processed. For now, the core observation is that the Lab’s works revealed the need to centralize many processes inside the corporate structure. We have confirmed that this technology is essential since it occurs across many different departments, and we already know that other departments will need OCR too.

So, currently, the success is that we get to know the processes and can work on changing and automating them.

On the other hand, we will also verify how expensive the different elements are to maintain this application with us. After all, we are a financial institution, so due to the data regulations we prefer a cloud-only provider. We would need to install the software directly on our servers, so we are verifying how much it costs to put up and maintain an environment for this application.

Lastly, we’ll also be evaluating the quality of the cooperation.

These are the elements that will affect the final summary.

Pekao Bank is one of the top banks in Poland, and it’s rare for such large entities to work with a start-up like Alphamoon. Is there a lot of space for corporations to collaborate with start-ups? Will this trend grow?

There is definitely space for this. Corporations are maturing to open up to new ventures, such as testing high-tech tools. They are also increasingly aware of the benefits from working with people with entirely different work ethics and mindsets. Our bank is evolving, aspiring to become the technology leader in the financial sector.

But one should remember the limitations existing in the world of finance too. By its nature, a start-up is an entity that is riskier than a mature company, that’s why we need to be careful with choosing start-ups to cooperate. Besides, we have a lot of restrictions to pay attention to in order to heavy regulations.

But as we mentioned earlier, time is essential. In finance, you have to show solid determination and explain employees how the start-up work – that’s it’s not a regular vendor or another corporation. Start-ups change depending on the market trends, they can often pivot and update their solutions to tap into new potential use cases. Our job is to mediate between these two sides – corporations and start-ups – and educate one about the other. It is about bridging two worlds and finding a common language. That’s also why this is an exciting project to be a part of.

How is the budget for implementing innovative solutions in banks allocated? What are the most critical factors influencing the go/no-go decision?

So far, we have operated in two ways.

One journey for working with start-ups was through accelerator partnerships. The accelerator program provided us with our funding – the start-up could use the grant to finance the pilot costs. And then we didn’t need to use our resources for testing. As a result, only in the case of the purchase, we required internal budget resources.

On the other hand, we also finance pilots with our own funds. We’ve had some that we’ve implemented from the laboratory’s funds, and we’ve also had this kind of budget for testing start-ups in the company. To have the so-called green light, we’d need to validate the start-up first and get a sense of its traction. For the last year and a half, we worked to show that these start-ups are stable, you can work with them, and they deliver value.

Each use case brings about several different document types. Do you see any of them that banks could automate easily?

Banks have a huge potential for automating documents, e.g., invoices.

There is a massive stack of documents that we can process faster – e.g., tax reports, certificates of earnings, and loan agreements. Business clients provide us with Income and Expense Ledgers, statements or balance sheets. Although our goal is to reduce paper usage, there are also situations when physical copies will never cease to exist, so document processing with OCR is critical here.

Do you see the potential for further collaboration with Alphamoon and expanding more areas or processes with automation?

We’re in the process of testing Alphamoon as a continuation of the acceleration program.This is still an early stage of validation of the tool; once we complete the pilot and see what effects Alphamoon will have on the two processes compared to the second startup, we will be able to make the final call.

Thank you so much for the interview.